Construction

Effective Credit Risk Management Solutions for Construction Suppliers

Leading-edge credit risk management solutions for companies selling to the construction and building industry, including leasing or hiring equipment, selling goods on credit and selling goods on cash terms. Onboard creditworthy customers, register security on PPSR, monitor for risk and collect invoices. Fast.

Make wise credit decisions, manage financial risk, and get paid

Construction is one of the highest risk industries for credit management, with the insolvency rate rapidly rising. Our products create a streamlined process from online trade applications and PPSR through to ongoing risk monitoring. The top features for the construction industry include automated construction license validation, industry-specific data from BICB, and one-click PPSR registrations.

Before Access Intell

After Access Intell

Automated construction license validation

Save time and ensure compliance with automatic validation of construction licenses. Easily ensure regulatory compliance both at the time of customer application and ongoing monitoring through the automated validation of a customer’s construction license.

Read our use case for more details on how construction suppliers manage credit risk by validating building licenses automatically.

Construction industry-specific data

Receive industry-specific data to inform wise decisions through integrated Building Industry Credit Bureau (BICB) credit reports and scores. *Members only

An accurate, efficient pPSR Process for you

One-click PPSR registrations are right every time with our pre-set profiles and built-in validation tools. This ensures your security is correct and enforceable as a priority. Plus you can save time and ensure accuracy with our bulk upload tool that automatically validates and corrects large volumes of registrations, discharges, transfers and renewals.

We’ll have you onboarded within 24 hours. Our flexible software integrates seamlessly with your unique business structure, processes and needs.

Our leading-edge products

The Access Intell products create a streamlined credit risk management process from online trade applications, PPSR, ongoing risk monitoring through to collections. Visit our product pages to learn more about their features and view interactive demo's.

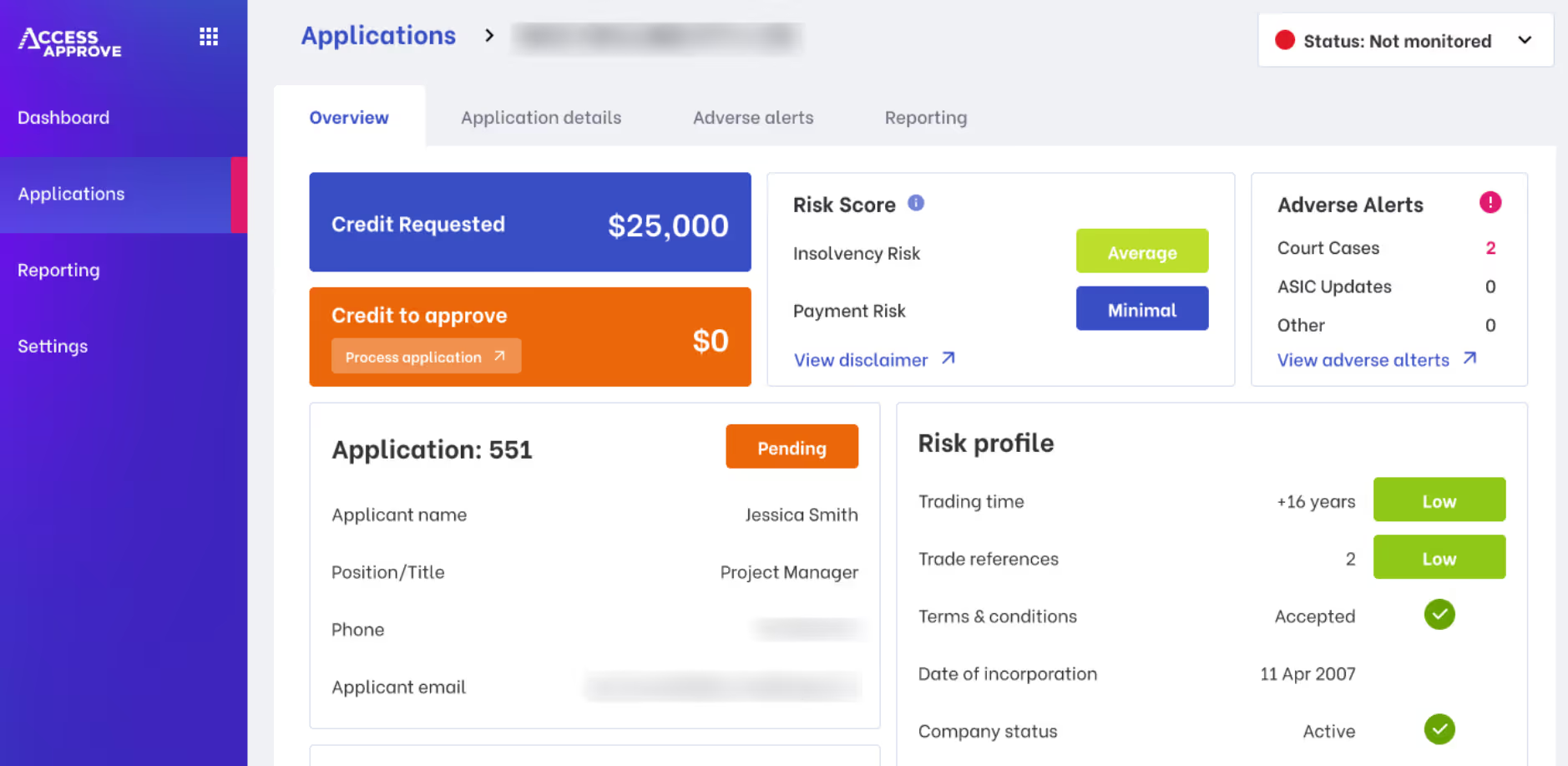

Onboarding

Our software gives you (and your customers) an efficient, paperless onboarding process. Receive, assess and approve trade credit applications online, seamlessly.

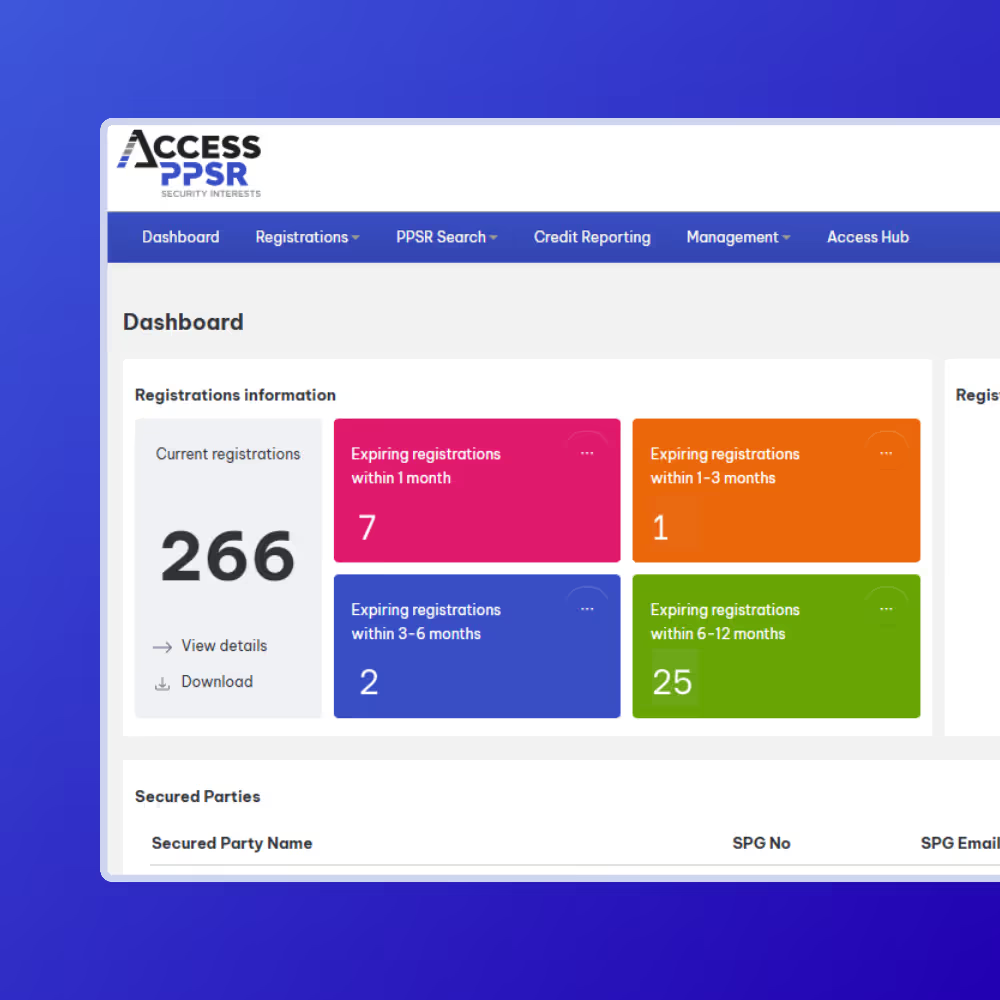

PPSR

Simplify the complexity of PPSR registrations through automation for an efficient, accurate process. In the event of customer insolvency, you're a secured creditor and are first in line for payment.

Monitoring

Continuously monitor the credit risk of your customers and be alerted to red flags for late payments and insolvency. All the information you need to proactively make decisions and manage credit is in one place, saving you time.

.avif)

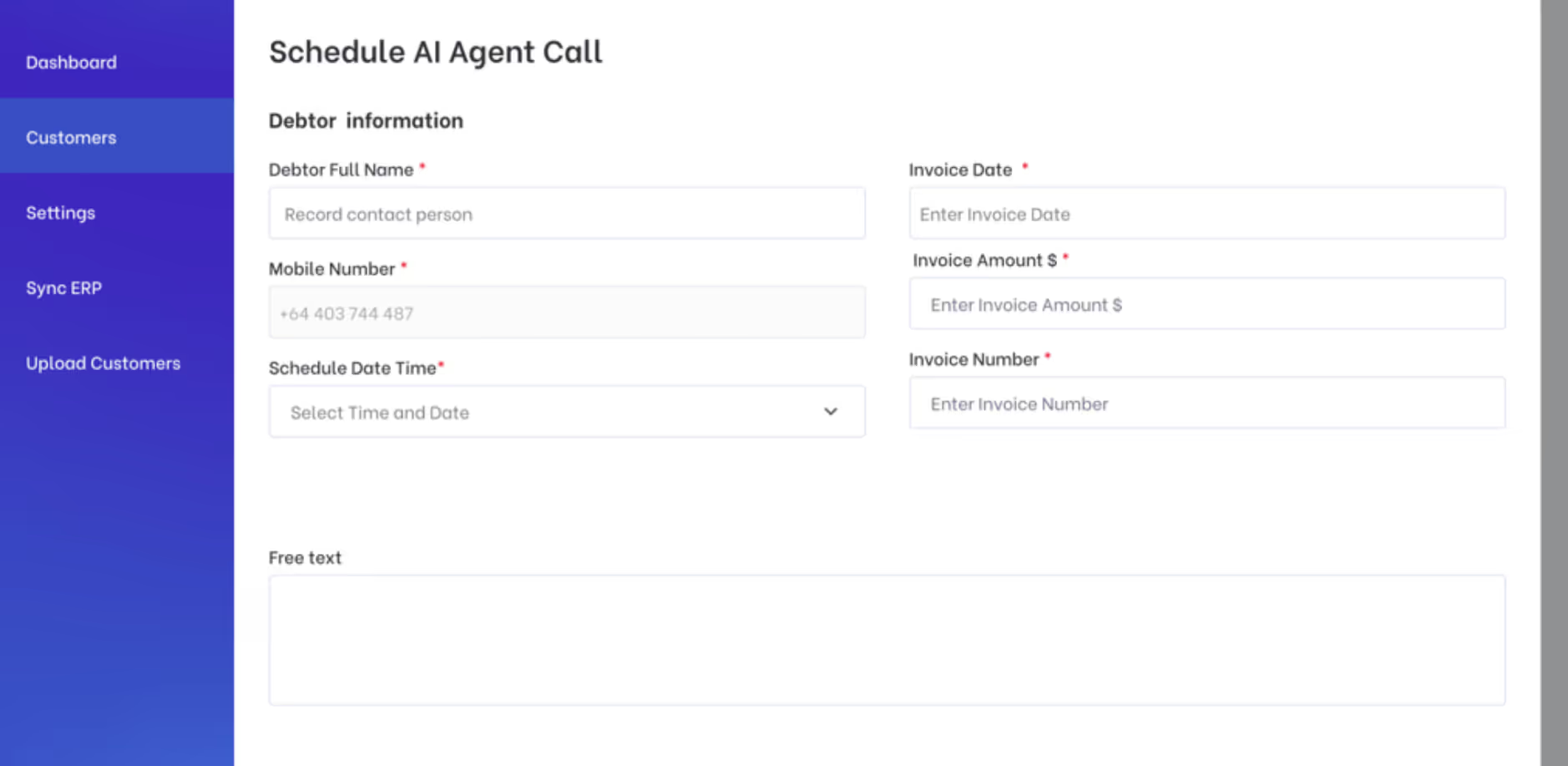

Agentic AI Collection Calls

Automate your accounts receivable calls with AI-Powered invoice reminder and collection calls. The customisable AI Agent completes personalised conversations so you get paid, faster. Human escalation triggers and compliance safeguards ensure an enhanced customer experience.

Case Studies

Learn how construction suppliers like yours are using our products to make wise decisions and grow sales.

AI helps business collect debts without sacrificing customer relationships

Online Trade Credit Application Speeds Up Customer Onboarding From Days To Hours

Reliance on outdated credit data lost this business $25,000

Client testimonials

Our clients say we go above and beyond – hear what they have to say.

Kim Hulme

National Accounts Receivable and Payable Manager, Ausco Modular

Jane Turner

Accounts Receivable, ABC Building Products

Paul Burgess

National Credit Manager, Steelforce Australia

Ready to make wise decisions?

Book a meeting with us to have a personalised discussion on how we can add value to your business.